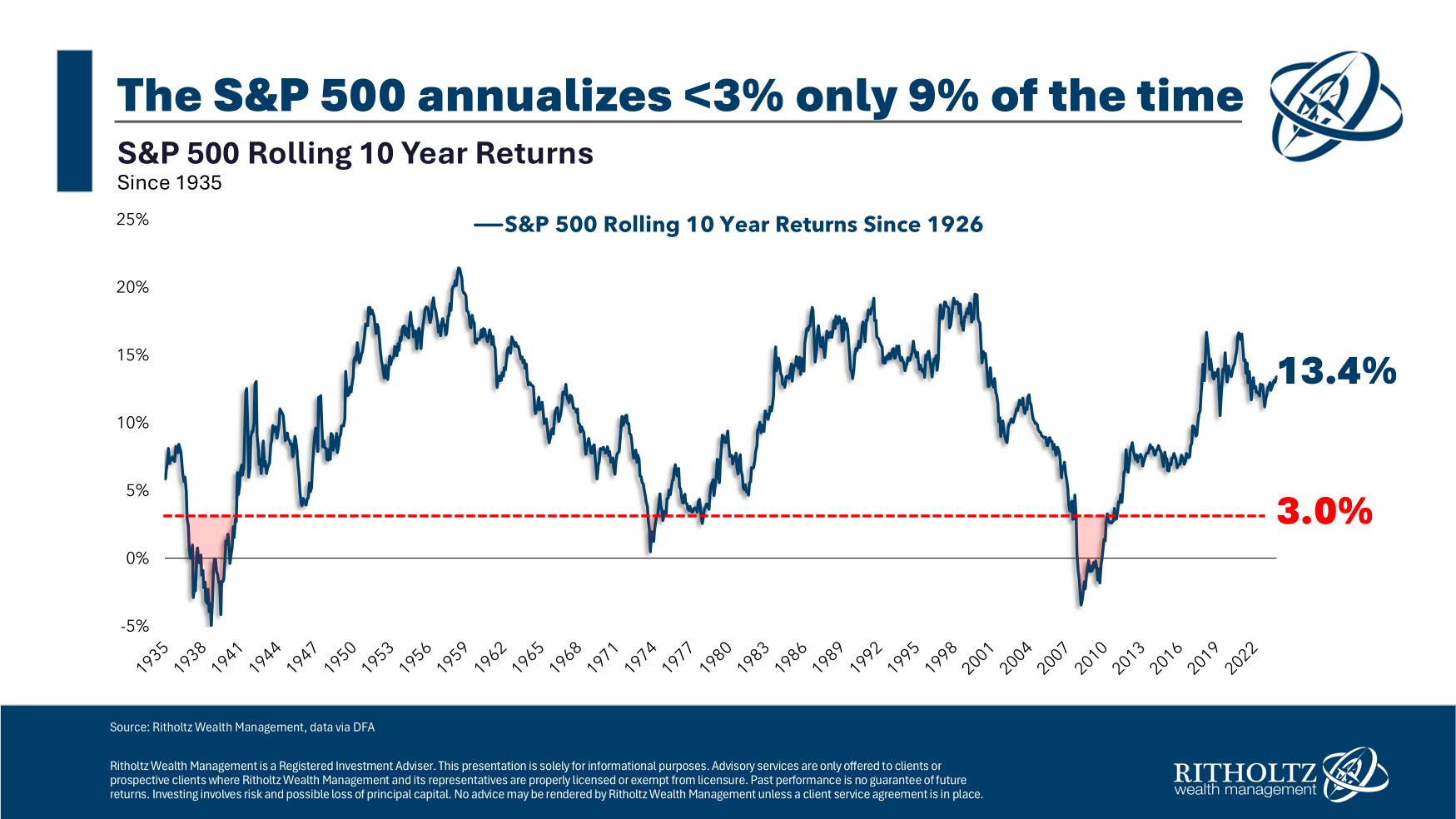

Thought I'd expand on two strategies that almost anybody can execute, but almost nobody does.

Either can have a huge impact on your financial position heading into retirement. Together, they can make your golden years truly golden.

Truly Maxing Out 401(k) or 403(b) Contributions

Above I mentioned maxing out your 401(k) / 403(b) contributions. Most of the people you heard at holiday parties holding forth on how they "maxed out" their 401(k) are talking about maxing out their employer's match.

That's a nice start. But for the vast majority of us, it's nowhere near enough for a comfortable retirement.

You need to max out the legal limit -- currently $23,500 up to age 50, $31,000 from age 50 to 60, and $34,750 from age 60 to 63 (thanks on that point,

@BamaNation...I wasn't aware of that new provision).

If you're early in your investing life, I know $23,500 seems an impossibly high number. And for most 30-year-olds, it is. But it doesn't have to be in your mid-40s. Here's how Mrs. Basket Case and I did it.

1. Have an honest conversation about needs vs. wants. You have to eat. You don't have to take the family out to dinner 3-4 times a week. You need a reliable car. You don't need a tricked-out electric F-150 new off the lot. You need a social life. You don't need a $500 a month country club membership, with a $2,500 set of golf clubs, plus 10 rounds a month of golf cart fees, Nassau bets and 19th hole tabs. You need time off to re-charge. You don't need 10 days at Disney World staying at the Grand Floridian, eating at Victoria and Albert's.

2. After completing a tough assessment of needs vs. wants vs. income, start off with as much as you can make room to contribute.

Remember that your contributions are in pre-tax dollars. IOW, Uncle Sam pays part of your contribution. Suppose you're in the 28% tax bracket, and you put in $200 a paycheck. Your take-home is only $144 less than if you had contributed nothing at all. Yet your 401(k) balance goes up $200,

plus whatever match your employer makes.

Depending on your tax bracket and your employer's match, your first-year returns on each year's new money can easily reach well over 100%, maybe even 200%.

You can't get anywhere remotely approaching that return anywhere else, and are leaving tons of money on the table if you don't take advantage of this.

3. This is the hard part and it takes discipline. Every raise, whether through annual salary increases or promotions, goes into the 401(k). And you keep on doing that for as long as it takes you to reach the legal max.

I won't lie -- it's no fun. I didn't have a take-home raise for 8 solid years. But when I finally did, it was fantabulously glorious.

Plus, as BamaNation alludes, after 2-3 months, it kind of gets baked into your monthly cash flow and it's not as painful as you might imagine.

4. Keep on maxing out until the day you retire. The legal max increases every few years, so you'll have to increase accordingly. Believe me, your retired self will thank your young self every single day.

Pay Off Your Mortgage Early

Currently, 30 year mortgage rates are about 7%. So for a $250K mortgage, that works out to principal and interest of $1,663. Over 30 years, you pay 360 x $1,663 = $598,680.

Note: This is principal and interest only. It doesn't include taxes and insurance.

Suppose you want to be done in 20 years. A lot of people think you'd have to pay 1.5x your 30 year payment. You don't. First, the 20 year interest rate is a bit lower (6.5% or so today). Second, exponential arithmetic works in your favor.

Together, that means that a $250K mortgage at 6.5% for 20 years works out to a payment of $1,863. Over 20 years, you pay $447,120 -- a savings of over $150,000. And 10 fewer years of making payments.

One neat trick: You can pay more than the required payment on your mortgage. If you do that, the extra reduces the outstanding principal. On a 30 year mortgage at today's rates, that's a guaranteed return of 7%.

Where else are you going to find a mathematically guaranteed return of 7%?

Mrs. Basket Case and I did this:

1. We started with a goal of being finished with mortgage payments after 15 years.

2. We agreed that we might trade up houses over time, but 15 years from the

original start date, we'd be done.

So suppose 3 years into the plan, we had our eye on a new house. We'd have to have that house paid off in 12 years -- 15 years from the original start date, less 3 years elapsed time. If we couldn't afford that, we couldn't afford the house.

3. We actually had mortgage notes on a 25 year amortization schedule. But we took advantage of the option to pay more. So we paid on a 15 year schedule -- or 12, or however many years we had left on the original plan when we bought the new house.

The cool thing about that was it gave us the flexibility to drop back to the lower contractually required payment in the event of a no-foolin' emergency. Sure, the interest rate was a tick higher, but not much. We just figured it was the price of having the flexibility if we needed it.

We were fortunate that we never had to use that option. But the fact that it was there was a source of peace of mind.

Both of these plans require discipline. You have to watch your friends have a big time spending, spending, spending, hear them brag about their stuff or where they just ate or went on vacation, and listen to them laugh and shake their heads at you.

Then one evening when you're a few months from retirement, you'll be at some cocktail party. You're talking about your plans, and they're moaning about having to work forever. They ask how you did it, and you tell them the two points above -- max out tax-advantaged retirement plans and pay off the house early. They'll look at you like you have three heads and say, "I remember you talking about that...but you really did it?!?"

It's sad to watch their faces as they realize that they're too far along in life to get their finances in order to retire in the way they want. I also have to confess to a bit of schadenfreude when I remember how much they mocked what the Basket Cases were doing.

Of all the assets you have as a young person, time is both the most valuable and the most perishible.

:max_bytes(150000):strip_icc()/GettyImages-1137410597-e4345c6c13b44b4e8886c47eb5d3d051.jpg)

")